KYC: What is it and How Does it Work?

What is KYC

KYC (Know Your Customer) is a process by which businesses verify the identity of their customers to prevent money laundering, identity theft, financial fraud, and terrorism financing. This process involves verifying your identity and address using government-issued documents (such as a driver's license or passport).

The purpose of KYC is to combat money laundering, terrorist financing, and tax evasion. Documents that verify the client's identity, such as a passport or other identification document, are used for verification. The set of data used in the verification procedure is established directly by the exchange platform.

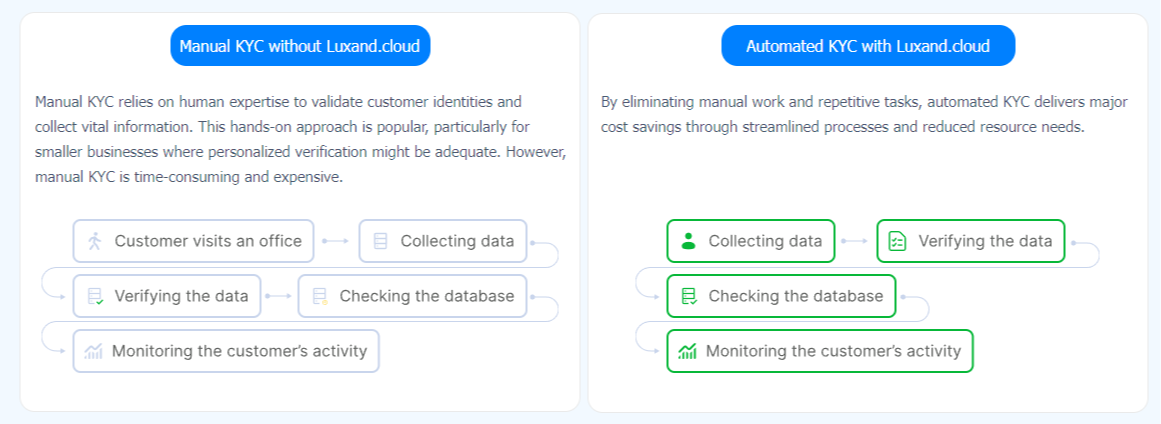

The process of verifying customer identities can be manual or automated. Manual KYC involves meeting with a representative of the company to verify your identity in person. Automated KYC systems typically use a combination of technologies to verify your identity remotely:

Optical character recognition (OCR). OCR software can autonomously interpret and extract data from documents, such as passports and driver's licenses.

Machine learning (ML). ML algorithms can detect and flag potentially fraudulent patterns in data, such as inconsistencies in customer information or fraudulent transactions.

Biometric verification. Biometric verification systems can employ facial recognition or fingerprint scans to validate a customer's identity.

Differences Between KYC and AML

KYC requirements are a part of a comprehensive Anti-Money Laundering (AML) program. AML includes various regulatory processes to counter financial crimes, such as software filtering, documentation tracking, and criminalization. KYC is an integral component of the AML process, involving personal data verification and enhanced due diligence.

KYC, AML, and other regulatory processes developed by authorities collectively make it more challenging for organized crime and terrorists to operate illegally. These measures prevent them from converting criminal proceeds into legitimate income. However, some members of the cryptocurrency community have a different perspective on this benefit and exhibit ambivalence toward KYC verification. They argue that KYC and AML contradict the concept of decentralization.

KYC in Different Industries

KYC is used in a wide variety of industries, including:

Financial services. KYC is a crucial practice in the financial services industry to combat financial crimes such as terrorism financing, money laundering, and fraud. It helps financial institutions verify their customers' identity and risk profile to ensure they are not involved in illicit activities.

Payment processors. Companies that process payments also integrate KYC checks to ensure that the money they are handling is not being used for illegal purposes.

Cryptocurrency exchanges. Cryptocurrency exchanges impose stricter KYC requirements compared to traditional financial institutions, primarily due to the anonymity associated with cryptocurrency transactions.

Gambling. Online gambling and gaming companies utilize KYC to verify the identity of their customers, aiming to prevent underage gambling and fraudulent activities.

Face Recognition in KYC

Face recognition technology is rapidly gaining traction in the digital onboarding and KYC landscape, offering a secure and efficient approach to verifying customer identities. Its integration streamlines the onboarding process, enhances security, and mitigates fraud risks, making it an attractive solution for businesses across various industries.

Here is how face recognition and liveness detection work in KYC, using the Luxand.cloud automated KYC solution.

More and more businesses across various industries are opting for facial recognition technology as part of their automated KYC processes — facial recognition enables users to verify their identity quickly and effortlessly, thereby enhancing the overall user experience and streamlining the onboarding process.

Moreover, manual document verification and in-person checks are often lengthy, labor-intensive, and costly. The facial recognition technology streamlines the identity verification process by automating it, eliminating the need for manual intervention, and significantly reducing both costs and processing time.

Facial Recognition Benefits for KYC

As mentioned earlier, automated KYC can be based on OCR, machine learning, or biometric verification. While all these methods are effective, facial recognition, as a part of biometric verification systems, is more widely used nowadays due to the various benefits it provides. Here are some studies that highlight how facial recognition contributes to saving businesses money:

Expanded market reach by 10%. According to a study by Mastercard, facial recognition KYC expanded market reach by 10% for financial institutions.

Reduced fraud by 50%. A study by Thales found that facial recognition KYC reduced fraud by 50% for banks.

Protected businesses from financial losses of $1 billion. EY found that facial recognition KYC protected businesses from financial losses of $1 billion in the financial services industry.

Prevented identity theft by 70. FIS found that facial recognition KYC prevented identity theft by 70% for financial institutions.

Reduced the risk of financial losses. According to the Aite Group, facial recognition KYC reduced the risk of financial losses by 90% for businesses in high-risk industries.

Conclusion

In conclusion, facial recognition is the technology that makes the KYC process faster and more secure. More and more businesses from different industries choose facial recognition technology to integrate into their digital onboarding and automated KYC processes, as facial recognition helps streamline onboarding, enhance security, reduce fraud risks, and comply with regulatory requirements.